AI-Based Attacks,

Fraud Management & Cybercrime,

Fraud Risk Management

Similar Fraud Rates Across Documents Reveal Weaknesses in Verification Workflows

In a troubling trend for financial institutions, a recent report highlights that one out of every sixteen documents processed in the past year displayed evidence of manipulation, fabrication, or misrepresentation. While this alarming statistic often prompts fraud teams to seek improved document detection methods and tighter review processes, experts argue that the primary issue lies not within the documents themselves, but rather in the verification architecture that surrounds them.

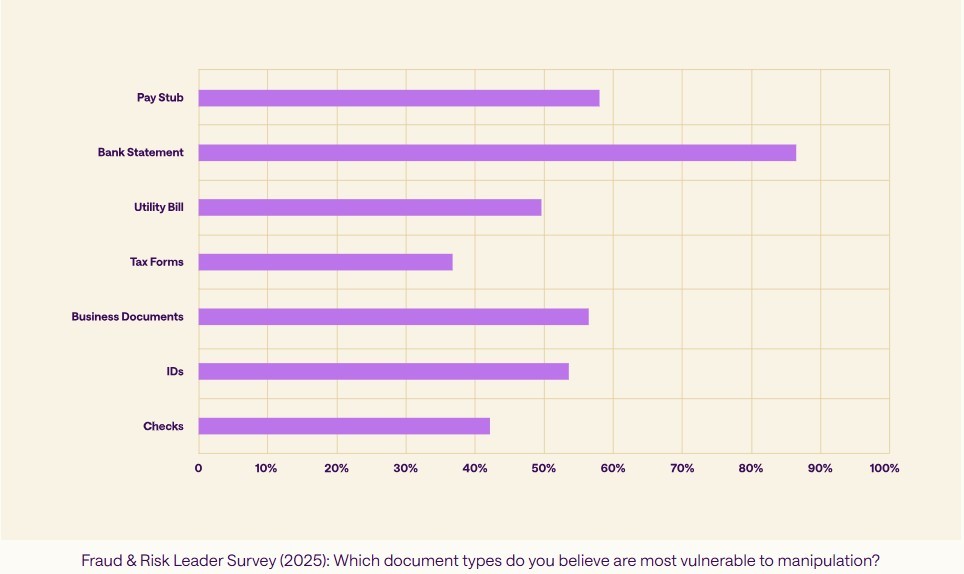

The findings from InScribe’s 2026 State of Document Fraud report indicate that rates of fraud are strikingly uniform across various document types. Whether considering bank statements, pay stubs, or tax forms, fraud rates oscillate between 4% to 7%. This uniformity suggests that fraudsters are not focusing on individual document categories as targets; instead, they are strategically probing the verification workflows of institutions to identify and exploit their weakest points.

With the landscape of fraud evolving more structurally, the report identified a significant increase in the percentage of documents demonstrating both identity and financial manipulation, which surged from 40.2% in 2024 to an alarming 59.8% in 2025. Fraudsters are adapting their strategies, moving away from merely submitting a single altered document to creating cohesive fraud packages. For example, a fake pay stub may be accompanied by a fraudulent bank statement and a manufactured employment letter designed to deceive verification systems that assess each document in isolation.

Utility bills, which might initially seem like less critical supporting documents, are revealing higher fraud rates compared to other document categories. This situation arises not from the documents’ inherent susceptibility to falsification, but from a perception problem among fraud reviewers, who tend to assign less scrutiny to secondary documents. Fraudsters have keenly capitalized on this oversight, seeking opportunities where the level of scrutiny is diminished.

This dilemma has been characterized by experts as the “architecture problem.” Essentially, financial institutions allocate scrutiny based on perceived document importance rather than recognizing the actual points of fraud pressure. When expectations regarding scrutiny diverge from points of vulnerability, fraudsters can easily navigate through these gaps. The current verification systems, which are generally designed to assess individual documents, are ill-suited for detecting broader fraudulent schemes that involve multiple documents.

Addressing this problem necessitates a fundamental rethinking of document verification within the larger context of risk management processes. Institutions must focus on creating a more comprehensive risk workflow rather than solely enhancing verification techniques.

Frank McKenna, Chief Fraud Strategist at Point Predictive, emphasizes that the industry’s approach towards fraud prevention is misaligned. He notes that the vast majority of applicants are honest individuals, stating, “Fraud is still a relatively rare event.” Consequently, the friction applied to filter out potential fraudulent applications should be limited to a small subset. However, many lenders tend to request pay stubs from all applicants, even though statistically, less than 10% of applicants are misrepresenting their income. This overarching tactic unjustly burdens the honest majority while marginalizing the few dishonest applicants.

Looking ahead, McKenna anticipates a transformative shift in how fraudsters operate, particularly with the rise of artificial intelligence capabilities. He warns that the emergence of AI-generated synthetic identities will enable scammers to create thousands of fake identities daily. By selecting ideal combinations of stolen Social Security numbers and other details, they can construct identities that blend seamlessly into legitimate records. This degree of sophistication poses an extraordinary challenge for banks, requiring them to prepare for an inevitable surge in fraud that far surpasses current levels.

The implications of these findings are significant for financial institutions still relying on traditional document-by-document verification methods. The warning is clear: the mechanisms that are currently in place are already vulnerable. The pressing question remains whether banks and lenders will take proactive measures to redesign their verification architecture before fraudsters completely exploit existing weaknesses.